Best Bank Accounts and Cards for Living Abroad Full Time

My Exact Setup

Some of the links on this page are affiliate links. This means I may earn a small commission if you decide to book through them — at no extra cost to you! Your support helps me keep this blog running, so a big thanks if you use them.

You’ve probably had the same bank account since you were a teenager, heck, maybe your parents set it up for you. You know how it works: card goes in, money comes out, bill gets paid. Simple.

It works the same way abroad, right?

Technically yes. But if you’re not strategic about it, fees will quietly drain hundreds of dollars a year from your account… And when you’re living abroad full time, not just visiting for two weeks, those small costs compound fast across every coffee, every grocery run, every ATM withdrawal, every rent payment.

I learned this the hard way. The first time I tried to wire a deposit for my first apartment abroad I got hit with $75 in transfer fees I never saw coming. (If you’re still figuring out how to find a place abroad, I wrote about that here — How to find an apartment abroad.)

That was enough to make me rethink my entire financial setup. Here’s what I use now and why each piece exists.

The Problem With Your Existing Setup Abroad

Your average U.S. credit card charges around 2.5% in foreign transaction fees on every purchase made outside the country. On a coffee that’s nothing. On a month of rent, groceries, transport, and meals, it adds up to real money.

Debit cards are the same story. Foreign transaction fees, dynamic currency conversion fees, and ATM withdrawal fees from non-U.S. banks stack up fast. What feels like a small charge per withdrawal becomes a real pattern when you’re living somewhere for months at a time.

And then there’s the stuff nobody warns you about. Sometimes certain cards don’t work in certain countries, and some places don’t take cards at all. In Morocco I had to keep texting my bank to confirm that yes, this purchase was actually me, then watched the transaction decline in front of a cashier anyway.

The solution isn’t one magic product. It’s a small stack of the right tools, each solving a different problem.

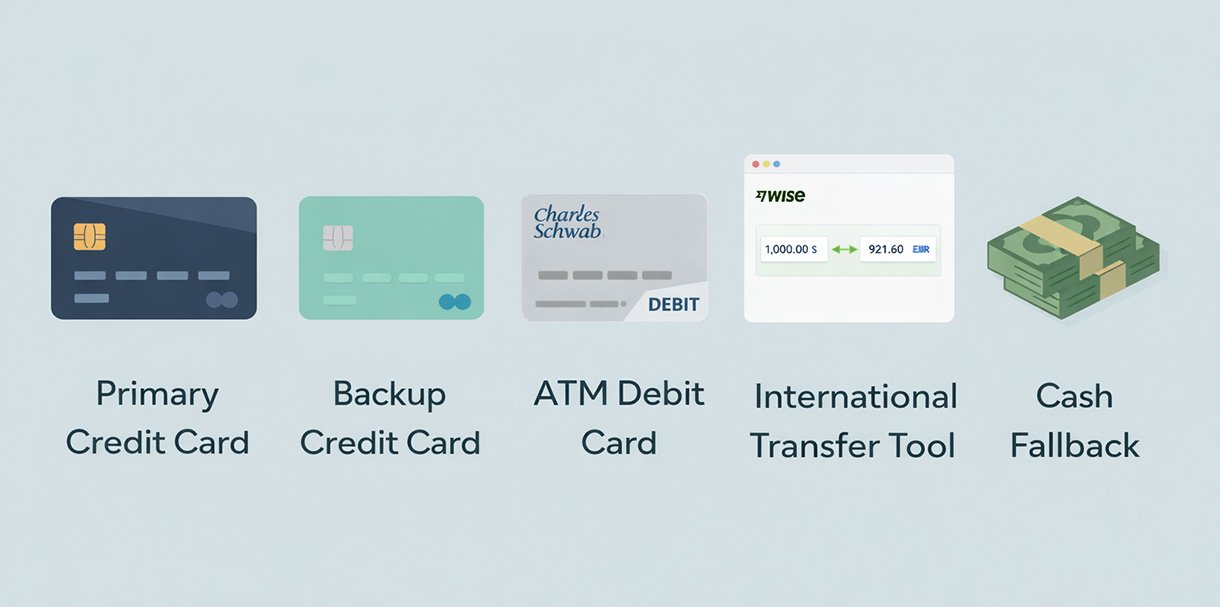

The Setup: Four Tools, Four Different Problems

1. A Premium Travel Credit Card + A No-Fee Backup

Problem it solves: Foreign transaction fees and travel benefits

The first thing I’d tell anyone moving abroad is to get at least one credit card with 0% foreign transaction fees. Ideally two. You always want a backup. Cards get frozen, declined, or just not accepted in certain countries. Having only one is a liability.

I pair a premium card with a no-annual-fee backup.

For my primary I use the Amex Platinum. Yes, it has a high annual fee, but for the way I live it more than pays for itself through:

- Priority Pass lounge access – genuinely useful when you’re moving between countries regularly

- Global Entry, TSA PreCheck, and CLEAR covered

- Annual travel credits

- Fine hotel benefits

- Travel insurance that’s actually comprehensive

The key detail: make sure whatever premium card you choose has 0% foreign transaction fees. Not all travel cards do despite marketing themselves as travel cards. Check before you apply.

For my backup I use the Apple Card. It has no annual fee, 0% foreign transaction fees, and offers cash back. It costs nothing to have and has saved me multiple times when my Amex wasn’t accepted.

2. Charles Schwab Checking Account

Problem it solves: ATM fees abroad

Standing at an ATM in Spain and seeing a €6.50 withdrawal fee on the screen was the moment I understood why this account matters. I put my card away, pulled out my Schwab card, and paid nothing. That’s the entire pitch.

The Charles Schwab High Yield Investor Checking account reimburses every ATM fee charged by any bank anywhere in the world at the end of each month. So even if a fee shows up on the transaction, it comes back. I’ve never thought about ATM fees since opening this account.

Everything else it does:

- No foreign transaction fees on purchases

- No monthly fees and no minimum balance

- Pays modest interest on your balance

- FDIC insured up to $250,000

The one thing to know before opening: you have to open a Schwab brokerage account first. You don’t have to use it or put anything in it though, it’s just required to access the checking account. It’s pretty quick to do.

One thing worth knowing: if you use my referral link and make a qualifying deposit into the brokerage account, Schwab will give you up to $1,000 depending on the amount you deposit. You don’t have to deposit anything to get the checking account — but if you’re moving money around before heading abroad anyway, it’s free money for doing something you were already going to do.

3. Wise

Problem it solves: International transfers and holding multiple currencies

The first time I tried to wire money to a foreign bank account, a deposit on my first sublet in Spain. After completing the transaction I got hit with $75 in transfer fees, which stung. That sent me straight to Wise.

Wise uses the mid-market exchange rate, it’s the same one you see when you Google a currency conversion. What’s nice is that it has transparent low fees instead of the hidden markups most banks quietly build in. No surprises, no $75 moments.

What I actually use it for day to day:

Paying the person renting their apartment to me directly is the main one. The process is simple: fast, cheap, and same-day in most cases. But my use of the card goes beyond rent. I’ve used Wise to pay for a Pantanal tour in Brazil when the operator didn’t accept foreign cards, settle a hotel bill in Brazil that wouldn’t take any of mine, and even set up my SmartFit gym membership in Colombia. Anything where you owe someone money in a foreign currency and your cards aren’t cooperating, Wise handles it cleanly.

If you’re going to be paying rent, splitting costs with people, or receiving money from abroad at any point, Wise is essential. The $75 transfer fee I paid before getting it was the last one.

4. Western Union. For When Cash Is Actually King

Problem it solves: Large cash needs in cash-dominant economies

Some countries don’t just prefer cash; they run on it. Argentina is the clearest example. When I was living in Buenos Aires, I’d often run into businesses wouldn’t accept cards at all, and the ones that did would actively offer you a discount for paying cash. That’s not a quirk, it’s a direct result of decades of currency instability and financial crises. When your country’s banks have been through that kind of whiplash, people tend to trust cash more.

Western Union handles larger cash needs in situations like this. It’s great when you need a meaningful amount of local currency and your usual setup isn’t the right tool.

One practical tip: your first transfer through Western Union typically comes with no fees, which is a nice perk.

The Setup at a Glance

| Tool | What it Solves | Cost |

|---|---|---|

| Amex Platinum + Apple Card | Foreign transaction fees, travel benefits, backup coverage | Amex annual fee, Apple Card free |

| Charles Schwab Checking | ATM fees worldwide | Free |

| Wise | International transfers, foreign currency payments | Free to open, low per-transfer fees |

| Western Union | Large cash needs in cash-dominant countries | Free first transfer |

What I’d Do Before Leaving the U.S.

Set all of this up before you go, not after you land somewhere and realize your card is getting declined or your transfer is costing you $75.

Specifically:

- Apply for a no-foreign-transaction-fee credit card and give it 2-3 weeks to arrive

- Open your Schwab checking account. Remember you need the brokerage account first

- Create your Wise account and verify your identity before you need to send money

The admin is boring. But it’s the difference between your financial life working seamlessly abroad and spending an afternoon on hold with your bank from a different timezone.

The Honest Takeaway

None of this is complicated once it’s set up. But most people don’t think about it until something goes wrong — a declined card, an unexpected fee, a transfer that costs three times what it should have.

The goal isn’t to find one perfect financial product. It’s to have the right tool for each situation: cards that don’t penalize you for spending abroad, a debit account that doesn’t charge you to access your own cash, a transfer service that doesn’t take a cut every time you pay someone, and a cash solution for the places that need it.

Set it up once, then stop thinking about it and go live your life.

Ready to Set Up Your Finances for Living Abroad?

Here are the tools I personally use and recommend:

💳 Amex Platinum — Premium travel card, 0% foreign fees 👉 Apply here

🍎 Apple Card — No annual fee, cash back, 0% foreign fees 👉 Apply here

🏦 Charles Schwab — Free ATM withdrawals worldwide 👉 Open account

💸 Wise — International transfers at the real exchange rate 👉 Sign up here

💵 Western Union — For cash-dominant countries 👉 Sign up here

Learn more about how to move abroad

-

Best Bank Accounts and Cards for Living Abroad Full Time (My Exact Setup)

Most people don’t think about their financial setup until something goes wrong abroad — a declined card, a surprise fee, a transfer that costs way more than it should. Here’s…

-

Google Fi for Digital Nomads: What’s Worked for Me Living Abroad Full Time

Living abroad full time sounds freeing until you realize how much of your life is still tied to a U.S. phone number. Here’s the setup I use to keep mine…

-

How I Choose the Right Neighborhood Abroad

How I Choose the Right Neighborhood Abroad What I look for in a neighborhood when I’m moving to a new city, from energy and livability to social life, convenience, and…

-

How I Find Apartments Abroad for a 1–6 Month Stay

How I Find Apartments Abroad for a 1–6 Month Stay What I look for in a place abroad, from neighborhood fit to walkability, wifi, and the details that actually make…